16 Oct Work Comp: How to Read an Experience Modification Worksheet

An experience modification rating (EMR) provides a numeric factor for adjusting insurance premiums.

An experience modification worksheet, often referred to as an experience rating worksheet or experience mod worksheet, is important in workers’ compensation insurance.

When a company receives an experience rating, it is accompanied by an experience modifier.

This experience modifier is a numerical multiplier applied to the annual premium, which can either increase or decrease the premium amount. Its primary function is to calculate a business’s experience modification rating (EMR), a numeric factor used to adjust insurance premiums based on the company’s historical record of workplace injuries and claims.

The experience modification worksheet allows both employers and insurers to evaluate and manage workplace safety, ultimately leading to fair and appropriate insurance premiums and safer working environments. This article provides an overview of the experience modification worksheet and delves into its elements.

Experience Modification Worksheet Overview

An experience modification worksheet serves as a repository of crucial workers’ compensation claims data, providing details on injury dates, types, claim payments and estimated future costs.

This data underpins the assessment of a company’s safety record and claims experience. Worksheets can look different depending on what rating bureau applies to the employer.

It is important to understand that the state a company is located in will determine how the modifier will be calculated. Some states use the National Council of Compensation Insurance (NCCI), and other states use independent rating bureaus that are created by the state statutes. States that are NCCI states will have their modifier calculated by the NCCI. States that are not NCCI states will have their modifier calculated by the rating bureau the state appoints to do so.

By comparing actual losses to expected losses derived from industry standards, the worksheet helps determine whether a business’s claims history is better or worse than the industry average. This EMR, once calculated, directly influences the cost of workers’ compensation coverage. With an EMR of 1.0 as the baseline, businesses with lower EMRs may enjoy reduced premiums, while those with higher EMRs may face increased costs, serving as a financial incentive for safety improvements.

Furthermore, the worksheet aids in risk management and budget planning and provides a basis for consultation and appeals if discrepancies or inaccuracies are identified. In essence, the experience modification worksheet is a pivotal tool for businesses to understand, manage and optimize their workers’ compensation insurance costs while promoting a safer workplace.

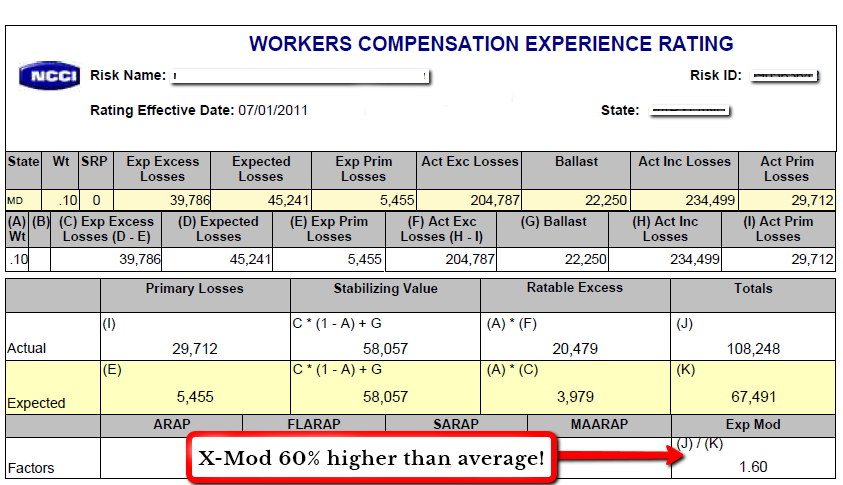

The worksheet has a specific layout where classification codes, payroll details and expected loss data are presented on the left side, while information related to claims is displayed on the right side. The initial six columns of this table provide various types of information. The first column, labeled as “Code,” denotes the classification codes assigned to a company.

Elements of an Experience Modification Worksheet

An experience modification worksheet typically contains several components. These components provide a comprehensive view of a company’s claims history and are essential for determining workers’ compensation insurance premiums. Here are the main components of an experience modification worksheet:

Basic information—This section includes essential details about the insured business, such as the company’s name, address, policy number and the effective date of the rating period. It also contains a risk identification number that is assigned to the employer by the NCCI. In addition, the worksheet will show “interstate” if the business operates in more than one state; it will list the state if it operates in only one state. Ensuring the accuracy of this information is critical for employers.

Policy period—The worksheet specifies the time frame for which the EMR is being calculated. This period typically spans three years but excludes the most recent policy year to ensure accurate historical data. The oldest policy period is at the top of the page, and the most recent is at the bottom of the page. Each policy period has a section for payroll that includes classification codes that identify the nature of the business. Employers can have one or more class codes that apply.

Claims data—The heart of the worksheet lies in the claims data section. This part includes comprehensive details about each workers’ compensation claim made by employees during the calculation period. Each claim entry typically includes the claim number, date of injury, type of injury, amount paid and the reserve amount.

Expected losses—The expected loss ratio (ELR) column typically provides information about the expected losses for the insured business. There is an ELR for each class code written out in dollars and cents. These expected losses are calculated based on industry standards and actuarial data and a state-by-state basis representing what an average business in the same industry would typically experience in terms of workers’ compensation claims. It serves as an indicator of the expected dollar amount that an insurer is likely to expend on losses for every $100 of payroll.

Experience modifier calculation—The EMR is calculated using a specific formula that compares the actual losses incurred by the business to the expected losses. While the exact formula may vary slightly, it generally follows a format similar to this:

Experience Modifier = (Actual Primary Losses + Expected Primary Losses) / Expected Primary Losses

- Actual primary losses—This is the total amount paid for all primary losses (direct claim costs) during the experience period.

- Expected primary losses—This is the expected amount of primary losses based on industry standards.

- Impact on premium—The calculation’s resulting EMR is a numerical factor applied to the company’s workers’ compensation insurance premium. An EMR of 1.0 is considered average, with values below indicating lower risk (leading to reduced premiums) and values above suggesting higher risk (increasing premiums).

- Risk classification—Some worksheets may include what the NCCI calls a discount ratio, or D-ratio. This determines the portion losses that are expected to be primary losses.

- Experience rating adjustment—This section may outline any additional adjustments or factors that affect the experience modifier. These adjustments could be state-specific, related to discounts or based on other factors.

- Loss data summary—Some worksheets include a summary table that provides an overview of actual losses, expected losses, and the resulting experience modifier. This summary can help stakeholders quickly assess the company’s claims history and EMR.

- Appeals and disputes—There may be information about the process for appealing or disputing the calculated EMR or claims data if a business believes there are inaccuracies or errors.

Conclusion

Understanding the components on the experience modification worksheet is crucial for businesses to manage their workers’ compensation insurance costs effectively and implement strategies to improve workplace safety and reduce claims. It is also essential to ensure that the EMR accurately reflects the company’s claims history, which, in turn, impacts insurance premiums.

Contact Barrow Group with any questions or to review your workers’ compensation documents.

Sorry, the comment form is closed at this time.